On May 19, 2026, the Solar Energy Association of Ukraine (SEAU) held an open meeting of its Legal Committee on the topic: “Dividends, Interest, and Royalties: How to Properly Make Payments Abroad.”

The event was held via Zoom and brought together business representatives, CFOs, accountants, tax consultants, lawyers, investors, and companies working with foreign partners and creditors.

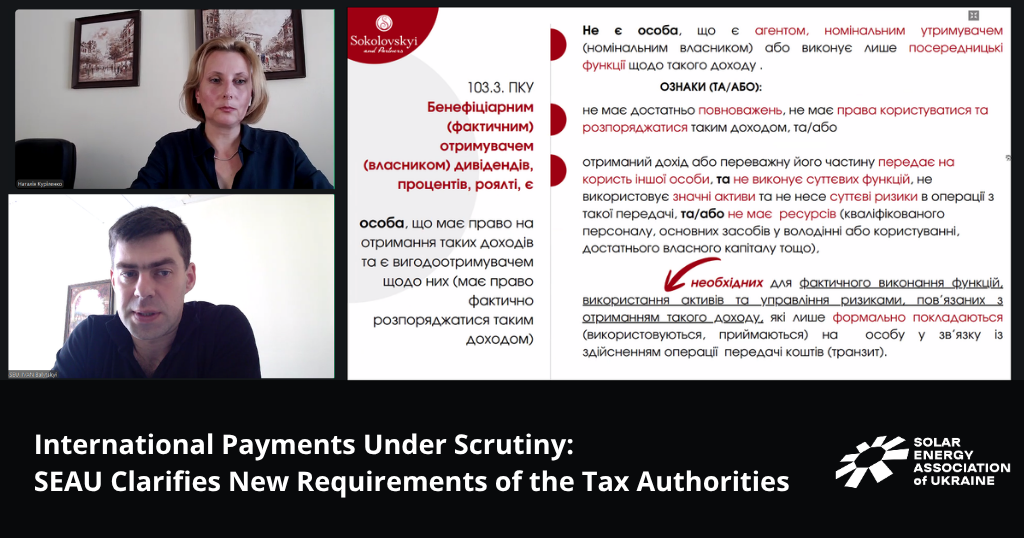

The meeting was moderated by Ivan Balytskyi, Chairman of the SEAU Legal Committee. The speaker was Nataliia Kurilenko, Head of Tax Practice, Auditor, and Attorney at Sokolovskyi & Partners Law Firm.

During the meeting, participants reviewed current taxation rules for dividends, interest, and royalty payments to non-residents, the application of international double taxation treaties, recent approaches of tax authorities, and the latest case law of the Supreme Court. Particular attention was paid to confirming beneficial ownership status, documentation requirements for international payments, and the risks associated with intermediary and conduit structures.

Opening the meeting, Ivan Balytskyi noted that the event continued a series of tax seminars organized by SEAU together with the Association’s principal legal advisor and partner, Sokolovskyi & Partners Law Firm.

In her presentation, Nataliia Kurilenko emphasized that recent changes in the approaches adopted by tax authorities and courts have significantly affected international payment practices:

“The changes in the taxation of income paid to non-residents are critical for taxpayers, as they have fundamentally changed the approach to this issue. Many companies, including large taxpayers, have already faced tax disputes due to the incorrect application of reduced treaty rates.”

The speaker reminded participants that the general withholding tax rate on payments to non-residents is 15%. However, double taxation treaties may provide reduced rates ranging from 0% to 15%, depending on the type of income and the recipient’s country of residence. The application of treaty benefits is only possible if several requirements are met, including the existence of a valid treaty, a properly issued tax residency certificate, and confirmation of beneficial ownership status.

A separate section of the meeting was devoted to the concept of the beneficial owner. Participants reviewed in detail the criteria used by tax authorities to determine whether a foreign company is the actual recipient of income, as well as indicators that may signal the use of intermediary or conduit structures.

Considerable attention was also paid to the practical implications of the implementation of the Multilateral Instrument (MLI) and the Common Reporting Standard (CRS) for the automatic exchange of tax information. As noted during the event, these instruments have significantly enhanced the ability of tax authorities to review international transactions, analyze cash flows, ownership structures, and the economic substance of foreign companies.

“Today, tax authorities have significantly more tools to analyze international transactions. Automatic exchange of information, international requests, and new approaches to determining beneficial ownership have effectively made most cross-border payments transparent. Therefore, businesses must proactively build a robust package of supporting evidence and documentation,” the expert emphasized.

The presentation also provided a detailed overview of the documents companies should maintain to substantiate their eligibility for treaty benefits. These include tax residency certificates, beneficial ownership declarations, corporate documents of the non-resident entity, financial statements, audit reports, bank statements, evidence of business activities, and proof of economic substance in the country of residence.

Nataliia Kurilenko also reviewed recent decisions of the Administrative Cassation Court of the Supreme Court, which demonstrate increasingly stringent requirements regarding proof of beneficial ownership status and the absence of conduit arrangements. Courts are increasingly examining not only formal documentation but also actual cash flows, income structures, staffing, office presence, assets, and genuine business activities.

During the Q&A session, participants discussed practical cases involving dividend, interest, and royalty payments, the application of international tax treaties, interaction with tax authorities, and preparation of supporting evidence to defend a company’s position in the event of a tax dispute.

Concluding her presentation, Nataliia Kurilenko announced several upcoming topics for professional discussion, including tax residency of individuals, Controlled Foreign Companies (CFCs), permanent establishments of non-residents in Ukraine, and taxation of real estate income.

SEAU continues its series of open and closed Legal Committee meetings aimed at improving the legal and tax awareness of energy market participants and providing businesses with practical tools for operating in a constantly evolving regulatory environment.